Moving to the USA? Learn why building credit is vital in the USA.

Most international students arrive in the U.S. with no credit history. This makes it very difficult to obtain a variety of essential services. In this article, we explain why it’s important to start building credit, and how to begin building yours upon arrival in the USA.

Students moving to the USA quickly learn that a U.S. credit score is vital for establishing themselves in the country. Without a local credit score or history, international students face a number of challenges, including getting approved for housing, credit cards, and difficulty buying, leasing or renting a vehicle or even getting a cell phone. If they are able to get approved, they typically end up paying high interest rates.

If you’re not familiar with the term “credit score,” it’s one that you will want to become familiar with during your time as an international student in the U.S. A credit score is a rating given to your financial background when assessed by a lender. When you’re applying to borrow money (like through a loan or credit card) the lender will most likely look at your credit score to see whether you are an eligible candidate.

Credit doesn’t transfer from one country to another.

As an expatriate relocating into the United States, you may not have official identification requirements like a social security number and a driver’s license. Without those essentials, it is almost impossible to establish credit.

Each country uses a different system for credit scoring, and credit does not transfer from country to country. Your credit score is what determines your creditworthiness to lenders. Since credit does not transfer from country-to-country, international students have a credit score of 0 when they first arrive in the U.S.To provide some perspective, the average American has a credit score between 600-700, and a good credit score is typically above 700.

Not having credit can make it hard to make much-needed purchases in your new country.

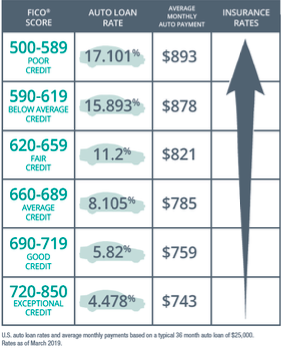

The chart below illustrates one example of how your credit score can affect an auto loan payment and insurance rates.

Your credit score is based on several factors.

Important transactions involve credit checks. Lenders require credit checks to obtain housing, car loans, home and auto insurance, and mobile phones. It is essential to understand what improves your overall credit score and to start building your score to give you better terms of those transactions.

In the United States, FICO®is the most common model for credit scoring, which was created by Fair Isaac & Company (FICO). Although there are competitor rating systems, this is the one you’re most likely to see during your time as an international student. A FICO®score is used to predict how reliable of a borrower you will be in terms of paying back the borrowed funds. However, typically if an individual does not have credit history that is at least six months old, they will not have a FICO®score. Additionally, different lenders will request your credit score from various sources depending on the system they use and whether they’ve adapted to the new FICO®system or use another company such as VantageScore.

When trying to build your credit there are five key factors1you need to know about that can impact your FICO®score:

1. Payment History (35%)refers to the repayments you have made on credit cards and loans in the past. Your credit score will take into consideration the speed and quantity of repayment on all the lines of credit you have taken out in the past to find the average.

2. Amount Owed (30%)The amount of your outstanding debt accounts for a large component of calculating your score. For example, does your credit card stay maxed out, or are you steadily paying it down?

3. Credit History Length (15%) The credit score will also take into consideration how long you have been building credit. If you start building credit responsibly when you are a student it will be reflected positively in your credit score. The sooner you start building your credit, the better.

4. New Credit (10%)Opening many new accounts in a short period of time suggests that you need additional forms of credit to make purchases. Using a few sources of credit wisely is better than having a large number that you can’t keep track of, or that are unnecessary.

5. Types of Credit in Use (10%)The different types of credit in your possession will be considered in your score, such as credit cards, loans and store cards. Having different forms of credit and using them responsibly can be beneficial in demonstrating how you manage your money in different areas.

Without a credit score, many establishments will not extend you credit, making it feel impossible to start building one.

So, how do you start building credit as an international student?

Open a bank account.

Check if the bank you work with in your home country has a U.S. branch near where you’re moving. If not, there are plenty of other options and your University might even have a bank on campus.

There are a couple of ways that you can build credit by using a bank account. Try opening both a checking and a saving account and regularly transfer money to your savings account if possible. This demonstrates that you’re responsible with your finances and you’re thinking long-term. It’s also a good idea to set up automatic or direct bill payments to ensure that your bills and expenses are paid on time. This is another way to demonstrate your financial responsibility, which helps build a strong credit score.

Pay utility bills.

If you are renting a property off campus you will most likely have to pay utility bills – gas, electric, phone, internet, etc. If you’re staying in on-campus accommodations you may not have all these utilities, but you will most likely need to apply for your own cell phone contract, which can also help you build credit. Making regular payments on all your utilities is another way to prove to lenders that you are responsible with your payments and will be a suitable applicant for a loan or credit option. For each of your utility bills you can request proof of your payments, which many credit providers will accept as supporting evidence of your payment background for your application.

Request store credit.

Store credit cards are used within that specific store. Just like a regular credit card, however, the store will charge you if you don’t make the payments on time. Additionally, although they’re usually easy to be approved for, store credit cards typically do not provide you with a credit limit as high as a traditional credit card. Therefore, it’s important to note that if you make minor purchases and don’t have a very high limit, your borrowed to available credit ratio could hurt your credit score.

How to get a credit card without a credit history or social security number.

Although having a credit card during your studies in the U.S. is important, it can be difficult to find a company that will allow you to open a credit card as a new international student- especially if you don’t have a Social Security Number (SSN) or credit history. However, there are some companies that will allow you to open a credit card as an international student without a SSN or credit history. Here’s how to start that process.

1. Apply for an Individual Taxpayer Identification Number (or ITIN)2

If you’re unable to get a Social Security number, you may still be able to apply for a credit card by using an Individual Taxpayer Identification Number, a tax-processing ID number assigned to individuals by the Internal Revenue Service.

Depending on the bank or credit card company, you can sometimes use an ITIN instead of a Social Security number when applying for a credit card. There are a few easy ways to apply for an ITIN.

- By mail.

- Through an IRS-authorized certified acceptance agentin the U.S. or abroad.

- At a designated IRS taxpayer assistance center.

After applying you should hear back from the IRS within a few weeks if you qualify and your application is complete.

2. Choose banks that accept an ITIN or alternative identification3

Credit card issuers aren’t required to ask for a Social Security number on the card application, but many do anyway. The good news is that some issuers will accept an ITIN instead. Here’s a quick rundown of issuers and where their policy currently stands on this:

|

Capital One |

Accepts ITIN or SSN only. Learn more. |

|

SelfScore Classic MasterCard |

Does not require a SSN or ITIN. Will request your passport, U.S. student visa, most recent Form I-20 and latest U.S. bank account statements. Available only to international students studying in the U.S. Learn more. |

|

Deserve |

No SSN required for International students. Credit limits up to $5,000, $0 annual fee & no foreign transaction fees and no security deposit or co-signer required. Learn more. |

3.Consider a prepaid card

If you can’t yet get approved for a credit card but still want a safer and more convenient way to pay than cash, a prepaid card could be the answer to your prayers — or at least a good payment alternative in the meantime.

While they aren’t technically credit cards, prepaid cards offer a way to keep your money in one place and pay with plastic when that’s the best and easiest option. Prepaid cards can be used in the same ways you might use a traditional credit card — to pay bills online, dine out or book an airline ticket.

The only drawback is you generally can’t build credit with a prepaid card, because your payment history typically isn’t reported to the major credit bureaus.

Financing or leading a vehicle.

Being new to the U.S. can come with a number of challenges when it comes to building credit and getting around. That where we come in, however. IAS can help you start building credit and driving record when relocating to the U.S. Our exclusive vehicle financing and leasing programs view you as a privileged customer starting with a high credit rating and safe driving record, allowing you to get the car you need while also building your credit record and driving history.

We are the vehicle experts for expats.

IAS helps you prepare and plan for your move by getting you behind the wheel so you can be productive and focus on what you are here for your studies. Our expertise in the automotive industry has helped over 50,000 foreign nationals get settled into their new countries, careers, schools, and internships with a vehicle that fits their needs.

Our Product Specialists are expert consultants, trained to identify your needs and use their extensive knowledge of the automotive market to find the right vehicle for your lifestyle and budget.

Sources:

1. “What’s in my FICO® Scores”https://www.myfico.com/credit-education/whats-in-your-credit-score

2. “How do I apply for an ITIN?” https://www.irs.gov/credits-deductions/individuals/how-do-i-apply-for-an-itin

3. “How to apply for a credit card without a Social Security Number” https://www.creditkarma.com/advice/i/credit-card-without-a-social-security-number/

Brianna Saputo

Get matched to the best program for you

Let us know what you're looking for so we can find the best school for you.

Useful Articles

Check Out These Schools

University of Southern California - International Academy

$5,000—$10,000 Semester

The New York Conservatory for Dramatic Arts

$35,000—$40,000 Year

George Mason University

Typical cost per Semester: $35,000—$40,000

Portland Community College

Typical cost per Year: $10,000 — $15,000

University of North Georgia

Typical cost per Year: $15,000—$20,000

Start your U.S. adventure with Study in the USA

Learn About U.S. education financing, housing, and more

ARGO

Get your U.S. visa approved with the help of Former Visa Officers. Study in the USA has partnered with Argo Visa to streamline your U.S. visa application process. Together, we offer expert guidance from Former Visa Officers to enhance your applicatio...

CORT Furniture Rental Student Packages

Most U.S. apartments come unfurnished. Make your move easy with a student furniture rental package from CORT. Flexible lease terms. Delivered before you arrive. Starting at $99 per month.* *with a 12-month lease

Kaplan International Languages

Kaplan International Languages is one of the world’s largest and most diverse education providers, we’ve been helping students to achieve outstanding language results for over 80 years. Students can learn English, French, and German.

Resources

Learn about American culture and education direct from our experts at Study in the USA. Read more